Car Insurance Myths That Create Real Gaps in Your Coverage

Car insurance myths are expensive. Most of them sound completely reasonable, which is why they travel so easily. They come from lenders, from family, from a rep at an 800 number who had 15 minutes to close the sale. Drivers repeat them to each other, make real coverage decisions based on them, and don’t find out they were wrong until a claim gets denied or a bill arrives that nobody expected.

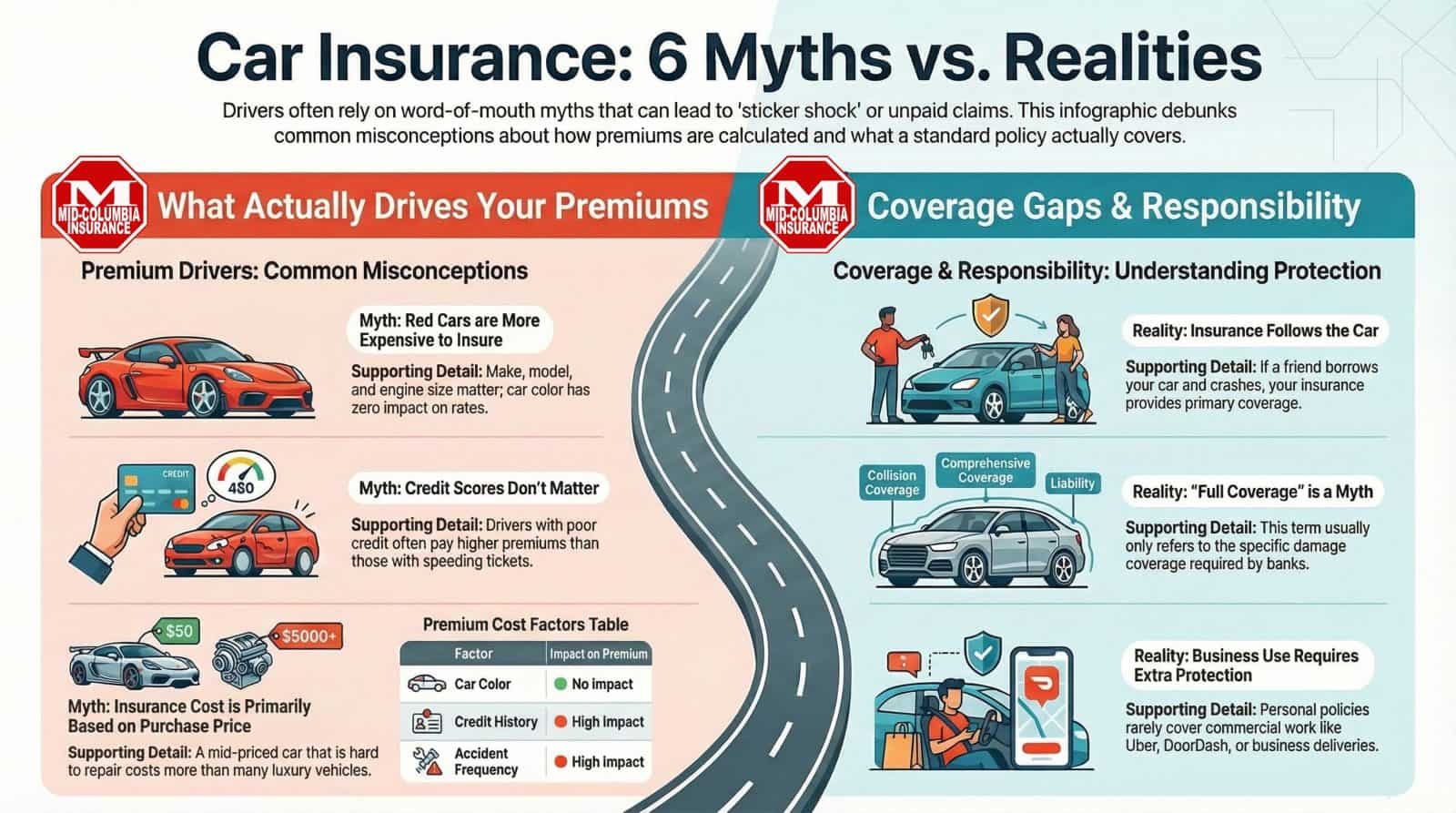

Here are ten of the most common ones, and what your policy actually says.

Myth: Full Coverage – What Banks Mean vs. What You Think

Full coverage is a term lenders created to describe a policy with both collision and OTC (comprehensive) physical damage protection on a financed vehicle. That covers their collateral. That’s where the definition ends.

Full coverage doesn’t cover personal property stolen from your car. It won’t pay off your loan if the vehicle is totaled for less than you owe. It doesn’t apply during rideshare or delivery driving. It’s a lender’s shorthand, not a policy type, and treating it like one is where the trouble starts.

Myth: Red Cars Cost More to Insure

Vehicle color has no effect on your car insurance rate. Insurers base rates on make, model, body type, engine size, model year and driver history. A red sports car costs the same to insure as a green one. A sports car costs more to insure than a station wagon, but that’s the vehicle class doing the work, not the paint.

Myth: Expensive Cars Cost More to Insure

A vehicle’s repair cost and accident frequency by model are bigger rating factors than sticker price. Premium calculations are built on how often a specific vehicle gets into claims and how much those claims cost to settle. A mid-priced car that’s expensive to fix or that’s driven disproportionately by higher-risk drivers can cost more to insure than a luxury vehicle typically driven by more experienced, lower-claim drivers. Check the insurance rate on any vehicle before you buy it, not after.

Myth: The Driver’s Insurance Covers an Accident

Liability coverage attaches to the vehicle, not the person operating it. When someone borrows your car and causes an accident, your auto insurance policy is primary. Their coverage is secondary and only engages after your limits are exhausted. Your deductible applies. The claim goes on your record.

Lending your keys to a driver with a poor history is underwriting risk you take on personally.

Myth: Your Loan Will Get Paid Off if Your Car is Totaled

Actual cash value is what an insurer pays when a vehicle is totaled: the depreciated fair market value at the time of the loss. Not the purchase price. Not the loan balance. What the car is worth today.

On a newer financed vehicle, that number is frequently less than what’s still owed. GAP insurance covers the difference between the insurer’s payout and the remaining loan balance. Without it, you owe the lender whatever the settlement check didn’t cover, and you have no vehicle. Lenders require collision and OTC coverage as a loan condition. They don’t require GAP insurance, which is why most drivers don’t have it.

Myth: Not-At-Fault Accidents Don’t Count as Claims

At-fault accidents earn a surcharge. Not-at-fault accidents don’t trigger the surcharge, but they can still cost you the accident-free discount you’ve been accumulating. Insurers base that discount on claim history, not fault determination. Being involved in a not-at-fault claim can cost more in lost discounts than the claim paid out. Talk to your agent before filing. Paying out of pocket rather than filing a police report or a claim for minor losses sometimes makes more financial sense

Myth: Letting My Coverage Lapse Will Save Me Money

Insurance lapses are treated as a risk signal by carriers. When you reinstate after a break in coverage, your new premium is typically higher than the rate you left. The increase over the following year often wipes out whatever was saved during the gap, before factoring in the exposure if something happened while you were uninsured, or the citation for driving without coverage.

Don’t drop your policy without running the actual math first.

Myth: Stuff In My Car Is Covered By My Car Insurance

Personal property stolen from your vehicle is excluded from your auto policy. Renters insurance and Homeowners insurance cover it the same way those policies cover items stolen from your home. If you don’t carry renters or homeowners insurance, that loss is yours entirely.

Your laptop, camera or tools in the back seat are not a car insurance problem. They never were.

Myth: Your Car Insurance Covers Business Use of Your Car

Business use is excluded from most personal auto policies. Driving for a rideshare platform, making deliveries or using your car as a regular part of your job creates a coverage gap that your personal policy won’t fill. The platform’s own insurance has limitations too, particularly between rides or during the delivery wait period. A commercial endorsement or rideshare add-on closes that exposure, but it has to be requested and added to your policy intentionally.

Truth: Mid-Columbia Insurance – Your Trusted Insurance Broker

Most of these problems are fixable with a policy review before anything goes wrong.

“The drivers who get caught unaware are the ones who didn’t know what they didn’t have,” says Gary Paulson of Mid-Columbia Insurance. “By the time someone calls us after an accident, it’s too late to add the coverage they needed.”

An independent agent reviews your full policy, not just the price on a comparison site. That review might catch missing GAP insurance, an absent renters insurance policy, excluded business use or liability limits that haven’t kept pace with your assets.

Call Mid-Columbia Insurance at (509)783-5600 or click “Get a Quote” to request a quote on your insurance. We serve drivers across Washington State as an independent agency with access to multiple carriers with no obligation to favor any single one. Our goal is to get you the insurance you want at a price you can afford!