Get A Free Auto Insurance Quote – Cheap Car Insurance Quotes

Call Now for Quote!

Free Auto Insurance Quotes – Cheap Car Insurance Quotes

Cost-effective auto insurance is a Mid-Columbia Insurance specialty. We can help you obtain free auto insurance quotes from multiple insurance companies and discover that cheap car insurance is available to you.

Mid-Columbia Insurance offers comprehensive coverage options tailored to your specific needs, ensuring your peace of mind on the road.

Join our community of savvy drivers today and discover how much you can save with our exclusive discounts and expert tips to lower your car insurance cost.

Key Takeaways

- Auto insurance coverage provides financial protection and peace of mind for vehicle owners.

- Money saving strategies include comparing quotes, looking for discounts, increasing deductibles, and reviewing coverage options.

- Understanding auto insurance coverage options is crucial for making informed decisions.

- Mid-Columbia Insurance can provide multiple car insurance quotes.

How Much Can You Save?

Having the correct auto insurance coverage is crucial but it’s also important to find ways to save money on your car insurance.

Comparing quotes from different insurance companies gives you a better understanding of the options available and allows you to find the most affordable premium.

Taking advantage of available discounts and choosing a higher deductible can help lower your car insurance rate and reduce your annual cost.

Request An Auto Quote

Disclaimer: By requesting a quote, I am providing my express written consent to Mid-Columbia Insurance to work up an insurance quote for me and to contact me by phone, text message, and email at the phone number and email address provided. Additionally, I acknowledge that I have read, understood, and agree to Mid-Columbia Insurance’s Privacy Policy.

Importance of auto insurance coverage

Auto insurance coverage is an essential safeguard for vehicle owners, providing financial protection and peace of mind. It is important to understand the different types of coverage available and their significance.

Liability coverage is crucial as it protects you in case you cause an accident that results in injury or property damage to others.

Comprehensive coverage is essential as it covers damage to your vehicle caused by incidents other than collisions, such as theft or natural disasters.

Collision coverage is vital as it pays for damages to your vehicle resulting from a collision with another vehicle or object.

Save money on your car insurance

To maximize savings on your car insurance, it is important to explore various strategies and discounts while considering your coverage needs.

One of the best ways to start is by getting free quotes from different insurance providers. By comparing quotes online, you can find affordable car insurance that fits your budget.

Look for discounts such as safe driver discounts, multi-policy discounts, or discounts for having certain safety features in your vehicle. Additionally, increasing your deductibles can help lower your premiums.

Remember to review your coverage options carefully to ensure you have the right amount of protection for your needs. Understanding the different aspects of auto insurance coverage is crucial in making informed decisions about your policy.

Lastly, uninsured/underinsured motorist coverage is important as it protects you if you are involved in an accident with someone who doesn’t have insurance or doesn’t have enough coverage.

Having adequate auto insurance coverage ensures that you are protected financially and legally in case of unforeseen circumstances.

Understanding Auto Insurance Coverage

When it comes to auto insurance coverage, it’s important to understand the different options available.

This includes liability coverage, comprehensive coverage, collision coverage, personal injury protection, and uninsured motorist coverage.

Many people have common questions about what these coverages entail and what benefits they provide.

Explanation of different coverage options

Understanding the various coverage options of auto insurance is crucial for obtaining the right protection for your vehicle. When it comes to auto insurance, there are several coverage options to consider.

- Liability coverage is mandatory in most states and protects you financially if you cause an accident that results in injury or property damage to others.

- Personal Injury Protection / Medical Payments coverage helps pay for medical expenses for you and your passengers in the event of an accident.

- Uninsured/Underinsured Motorists coverage protects you if you are involved in an accident with a driver who lacks insurance or has insufficient coverage.

- Comprehensive coverage provides protection against theft, vandalism, and other non-collision-related damages.

- Collision coverage, on the other hand, helps cover the cost of repairs or replacement if your vehicle is damaged in a collision.

- Other coverage options include rental reimbursement, roadside assistance, and gap insurance.

When comparing insurance quotes, it’s important to understand these coverage options and choose the ones that best suit your needs and budget. By understanding the coverage options available to you, you can make informed decisions and ensure that you have the right level of protection for your car.

Common questions about car insurance coverage

One important aspect of understanding auto insurance coverage is knowing the answers to common questions about different types of car insurance. Here are three common questions that people often have:

- How are insurance premiums calculated? Insurance premiums are determined by several factors, including the driver’s age, driving record, type of vehicle, and location. Insurance providers use these factors to assess the risk of insuring a particular driver and vehicle, which ultimately determines the premium amount.

- How can I get an online quote form? Most insurance providers offer online quote forms on their websites. These forms allow you to enter your information and receive a quote quickly and conveniently. Simply fill out the required fields and submit the form to get an estimate of your insurance rates.

- What are coverage limits? Coverage limits refer to the maximum amount your insurance provider will pay for a claim. It’s important to review your policy to understand the specific coverage limits for each type of coverage you have. Higher coverage limits generally result in higher premiums, but they provide more financial protection in the event of an accident or claim.

Benefits of having adequate coverage

Having adequate coverage for your auto insurance provides numerous benefits. It not only ensures financial and asset protection but also helps you comply with legal requirements and gives you peace of mind. With the right insurance policy, you can rest assured that you are covered in case of accidents or unforeseen events.

Here are some key benefits of having adequate coverage:

| Benefits | Description |

|---|---|

| Competitive rates | Adequate coverage ensures that you get the best rates for your auto insurance policy. |

| Discounts | Many insurance providers offer discounts for various factors such as good driving records. |

| Claims history | Having adequate coverage and a good claims history can result in lower premiums and better rates. |

| Deductible | Adequate coverage allows you to choose a deductible that suits your financial situation. |

Get a Car Insurance Quote

When it comes to car insurance, getting a quote is essential. It allows you to understand the cost of coverage and compare options from different companies.

Starting a car insurance quote is easy – you simply need to provide your personal information and details about your vehicle. From there, you can customize your coverage to meet your specific needs and budget.

Importance of getting a car insurance quote

Obtain a car insurance quote to ensure comprehensive coverage and competitive rates for your vehicle. Getting a car insurance quote is an essential step in protecting your vehicle and yourself from potential financial losses.

Here are three reasons why getting a car insurance quote is important:

- Understanding coverages: By obtaining a car insurance quote, you can gain a clear understanding of the different types of coverages available, such as uninsured/underinsured motorist coverage and personal injury protection (PIP). This knowledge allows you to make an informed decision about the level of coverage you need.

- Evaluating insurers: Getting a car insurance quote gives you the opportunity to compare different insurance companies. You can assess their reputation, customer service, and financial stability, ensuring you choose a reliable insurer that will be there for you when you need them.

- Personalized premiums: A car insurance quote allows you to receive personalized premiums based on factors such as your driving history, location, and the type of vehicle you own. This helps you budget effectively and find the most affordable coverage for your specific needs.

How to start a car insurance quote

To initiate the process of obtaining a car insurance quote, it is essential to begin by filling out an online form with accurate personal and vehicle details. This form will typically ask for personal information such as name, address, and contact details. It will also require details about your driving history, including any accidents or traffic violations you may have had. Additionally, you will need to provide information about your vehicle, including its make, model, and year of manufacture.

Age is another important factor that insurers consider when calculating premiums. Furthermore, it is important to indicate whether you want to include uninsured/underinsured motorist coverage in your policy. Once you have provided all the necessary information, you can proceed to the next step of customizing your car insurance coverage.

Customizing your car insurance coverage

After filling out the online form with accurate personal and vehicle details, it is important to customize your car insurance coverage to meet your specific needs. The right insurance coverage can provide you with peace of mind and financial protection in case of an accident or other unforeseen events.

Here are three key factors to consider when customizing your car insurance:

- Desired coverage level: Determine the level of coverage you need based on your personal circumstances and the value of your vehicle. This will help you choose the appropriate insurance policy that suits your needs.

- Coverage limits: Set the limits for liability coverage, which will determine the maximum amount your insurance company will pay for damages or injuries caused by an accident. Consider your assets and potential risks when deciding on these limits.

- Deductibles: Select a deductible amount that you can comfortably afford to pay out of pocket in case of a claim. A higher deductible can lower your premium costs, but make sure it aligns with your budget.

Comparing car insurance quotes from different companies

When comparing car insurance quotes from different companies, it is important to consider various factors to ensure you are getting the best coverage at the most affordable rates.

One effective way to compare quotes is by using quote comparison websites, which allow you to easily compare multiple quotes from different insurers side by side.

In addition to comparing prices, it is also crucial to evaluate the coverage options provided by each company. Look for insurers that offer premium discounts for safe driving, multiple policies, or bundling your car insurance with other types of insurance.

Online policy management is another important factor to consider, as it allows you to easily access and update your policy whenever necessary.

Reading customer testimonials and review ratings can provide insight into the level of customer service and satisfaction offered by different insurers.

By considering all of these factors, you can make an informed decision and find the right car insurance provider for your needs.

In the next section, we will discuss the various auto insurance discounts that can help you save even more on your premiums.

Auto Insurance Discounts

Auto insurance discounts are a great way to save money on your car insurance premiums. By understanding the different types of discounts available and how to qualify for them, you can potentially save a significant amount of money.

It is important to research and compare different insurance companies to see how much you can save with the various car insurance discounts they offer.

Understanding auto insurance discounts

The insurer’s policies outline the eligibility requirements and types of discounts available for auto insurance. Understanding these discounts can help you save money on your car insurance premiums.

Here are three key types of auto insurance discounts:

- Safe Driver Discount: Insurance companies often reward drivers who have a clean driving record with lower premiums. By practicing safe driving habits and avoiding accidents or traffic violations, you can qualify for this discount.

- Good Student Discount: If you are a student and maintain good grades, you may be eligible for a discount on your auto insurance. Insurance companies believe that responsible students are also responsible drivers.

- Vehicle Safety Features: Installing safety features in your vehicle, such as anti-theft devices, airbags, and automatic seat belts, can also qualify you for a discount. These features reduce the risk of theft or injury, making your car safer to insure.

Available discounts and how to qualify

To qualify for available auto insurance discounts, it is important to meet the eligibility requirements set by the insurer and take advantage of the various cost-saving opportunities offered. Insurers offer a range of discounts to reward safe driving habits and customer loyalty. By understanding these discounts and how to qualify for them, you can save money on your auto insurance premiums. Here are some common auto insurance discounts and how you can qualify for them:

| Discount | Qualification |

|---|---|

| Multi-vehicle discount | Insure multiple vehicles on the same policy |

| Defensive driving course discount | Complete an approved defensive driving course |

| Bundle discount | Insure your home and car with the same insurance company |

| Accident forgiveness | Maintain a clean driving record for a specified period of time |

| Claims-free discount | Go a certain period of time without filing a claim |

How much you can save with car insurance discounts

By taking advantage of car insurance discounts, drivers can save a significant amount on their premiums. Here are three ways you can save money with car insurance discounts:

- Compare car insurance quotes: By obtaining multiple quotes from different insurance providers, you can find the cheapest car insurance rates available. This allows you to choose the most affordable option that still provides adequate coverage.

- Look for auto insurance quotes that offer discounts for various factors such as having a car alarm. Many insurance companies offer discounts to drivers who have installed a car alarm. This discount can help reduce your premium and provide additional security for your vehicle.

- Fill insurance coverage gaps: Maintaining continuous car insurance coverage can help you save money. Insurance companies often offer discounts to drivers who have had continuous coverage without any gaps. By avoiding coverage lapses, you can qualify for lower rates and potentially save a significant amount on your premiums.

Tips to Lower Your Car Insurance Rate

There are several strategies you can implement to reduce your car insurance premium and save money. To help lower your car insurance rate, consider the following tips:

- Raise your deductible

- Maintain a clean driving record

- Choose your car wisely

- Bundle your insurance policies

- Install safety devices

- Compare insurers

- Take defensive driving courses

- Maximize discounts

- Regularly review your policy

Exploring these options can help you find ways to reduce your car insurance costs.

Factors affecting car insurance rates

One of the key factors in determining car insurance rates is the driver’s driving record and vehicle type. Insurance companies assess risk based on these factors, as well as several others, to determine the appropriate premium to charge.

Here are three factors that can affect your car insurance rates:

- Credit score: Insurance companies may consider your credit score when determining your premium. A higher credit score can indicate a lower risk of filing claims.

- Annual mileage: The more you drive, the higher your insurance rates may be. Insurance companies consider the likelihood of accidents and claims based on the number of miles you drive each year.

- Uninsured/underinsured motorist coverage: Having this coverage can protect you in case you’re involved in an accident with a driver who doesn’t have enough insurance. It may affect your premium depending on the coverage limits you choose.

Understanding these factors can help you navigate the world of car insurance rates. Now, let’s explore some tips to lower your car insurance rate.

Frequently Asked Questions

How Can I Compare Auto Insurance Quotes From Different Companies?

To effectively compare auto insurance quotes from different companies, it is essential to gather information on coverage options, deductibles, and premiums. Utilize online tools or consult with insurance agents to make an informed decision that aligns with your needs and budget.

What Factors Affect the Cost of My Auto Insurance Premium?

Several factors can influence the cost of your auto insurance premium. These include your driving record, age, type of vehicle, location, coverage options, and deductible. Understanding these factors can help you find the best insurance policy for your needs.

Can I Get Auto Insurance if I Have a Bad Driving Record or Previous Accidents?

Yes, it is possible to obtain auto insurance coverage even if you have a bad driving record or previous accidents. Insurance companies may consider these factors when determining your premium rates.

Are There Any Specific Coverage Options for High-Risk Drivers?

Yes, there are specific coverage options available for high-risk drivers. These options include SR-22 insurance, which is a certificate of financial responsibility, and non-standard auto insurance policies designed for drivers with a history of accidents or violations.

How Can I Qualify for Additional Discounts on My Auto Insurance?

To qualify for additional discounts on auto insurance, individuals can consider factors such as maintaining a clean driving record, bundling multiple policies, installing safety features in their vehicles, and belonging to certain professional organizations or alumni associations.

Conclusion

In conclusion, obtaining a free auto insurance quote and exploring cheap car insurance options can help you save money while ensuring you have sufficient coverage.

By understanding the different aspects of auto insurance and taking advantage of available discounts, you can lower your car insurance rate.

Don't miss out on the opportunity to protect your vehicle and finances – get a car insurance quote today.

What are You Waiting For?

Mid-Columbia Insurance represents companies like Safeco, National General, Dairyland, Progressive, Kemper Specialty, Foremost, Bristol West, and others that millions have come to know and trust.

Also, because of the number of companies we represent, we can insure most cars and drivers even if you are considered a high-risk driver. No matter if your driving record is Good, Bad, or Ugly, we can insure you.

What are you waiting for? Quit worrying about what would happen if you were in an accident or got pulled over by law enforcemnt. Pull out your cell phone and call us now at (509)783-5600 or Request A Quote here to get your free auto insurance quote right now.

- What Is a VIN (Vehicle Identifiction Number)?

- What is Uninsured Motorist Coverage?

- What is a Policyholder?

- What is Comprehensive Coverage?

- What is Collision Coverage?

- What Happens When an Excluded Driver Has a Car Accident?

- What is Full Coverage Car Insurance?

- Can someone drive my car if they are not on my insurance?

- Which type of car insurance is cheapest?

- Do I Need Auto Insurance To Drive A Car?

- Who Needs To Be On My Car Insurance Policy?

- What is Car Insurance?

Recent Car Insurance Posts

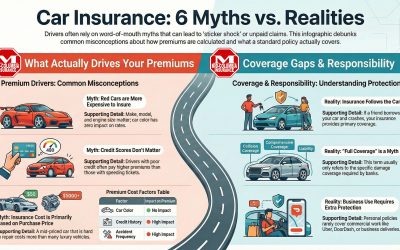

10 Common Car Insurance Myths and Misconceptions

Debunks auto insurance myths: color doesn’t affect rates, but credit and repairs do. Owners are liable in crashes, and “full coverage” is a misnomer. Consult agents for proper protection.

Is Uninsured Motorist Required in Washington?

Mid-Columbia Insurance wants to help get you cheap car insurance in Washington so that you can get the insurance you want at a price you can afford. We are familiar with Washington’s car insurance laws so you can be sure you’re meeting the minimum legal requirements....

Comprehensive Car Insurance Coverage Options

Comprehensive car insurance coverage shields you from financial loss due to non-collision events. It is optional if you own your car outright but most lenders require it to protect the loan.

How Much Is A No-Insurance Ticket In Washington State?

If you drive a car without insurance on Washington state roads, you could receive a no-insurance ticket and have to pay a fine of $550 or more.

Car Accident, Car Crash, or Traffic Collision?

“Car accident” implies that a collision is unpredictable or unpreventable, which is often not the case; “Car crash” is more informal and often used colloquially to describe a collision; “Traffic collision” is more accurate and does not imply cause, fault, or preventability.

Does a Lapse in Coverage Affect Your Car Insurance Rates?

If your car insurance has lapsed, you will probably loose a number of disounts and be required to pay more for your new insurance.

What Our Customers Are Saying About Us